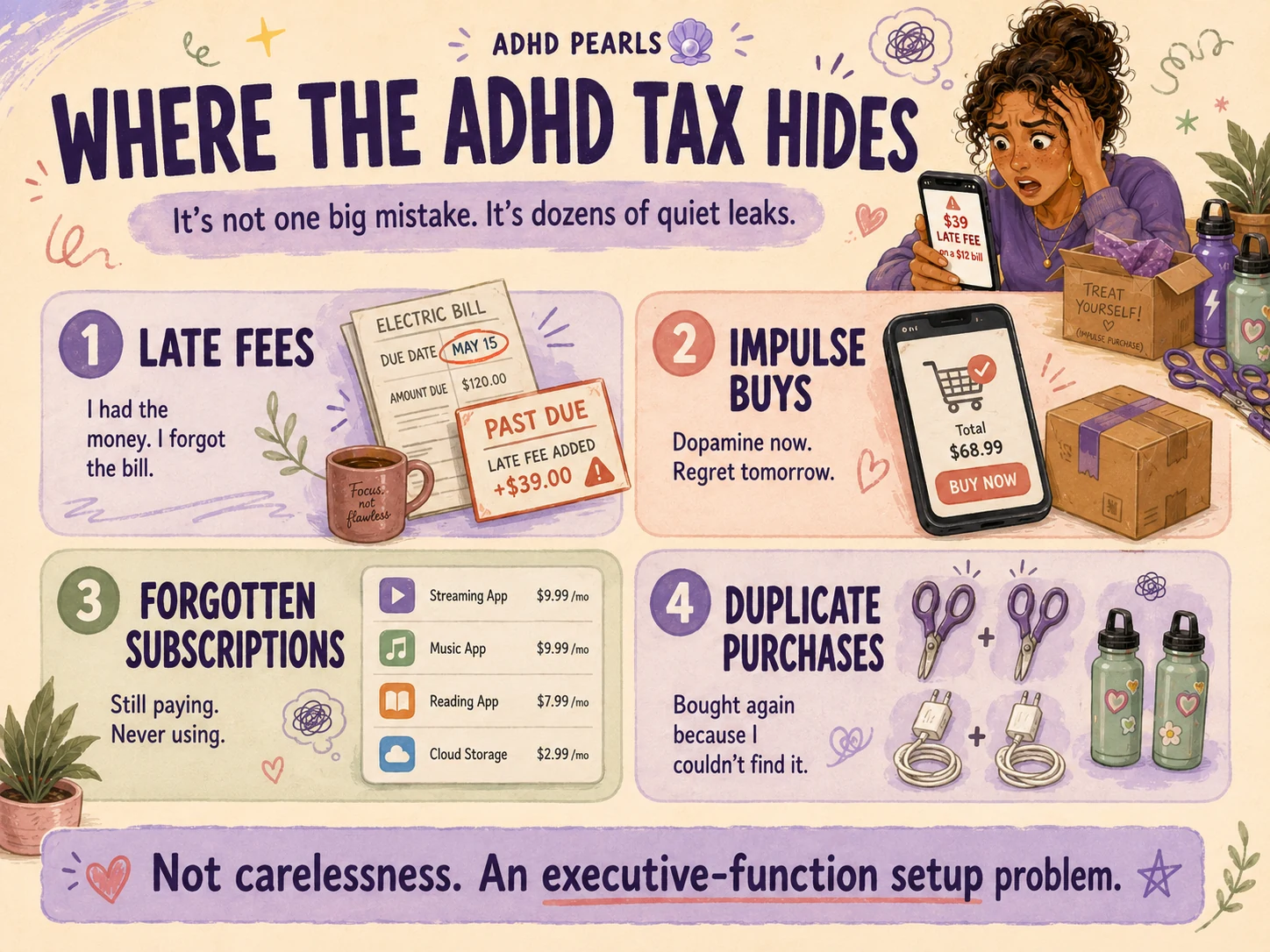

A few years ago I paid a $39 late fee on a $12 bill. I had the $12. I had the $39. What I did not have was any memory that the bill existed until the angry email arrived. The bill was never the problem. Remembering the bill was the problem.

That little leak has a name now: the ADHD tax — the money you lose not because you're broke or careless, but because of how ADHD plays out in real life. Late fees. Impulse buys. The free trial you meant to cancel in 2023. The fourth pair of scissors because you cannot find the first three.

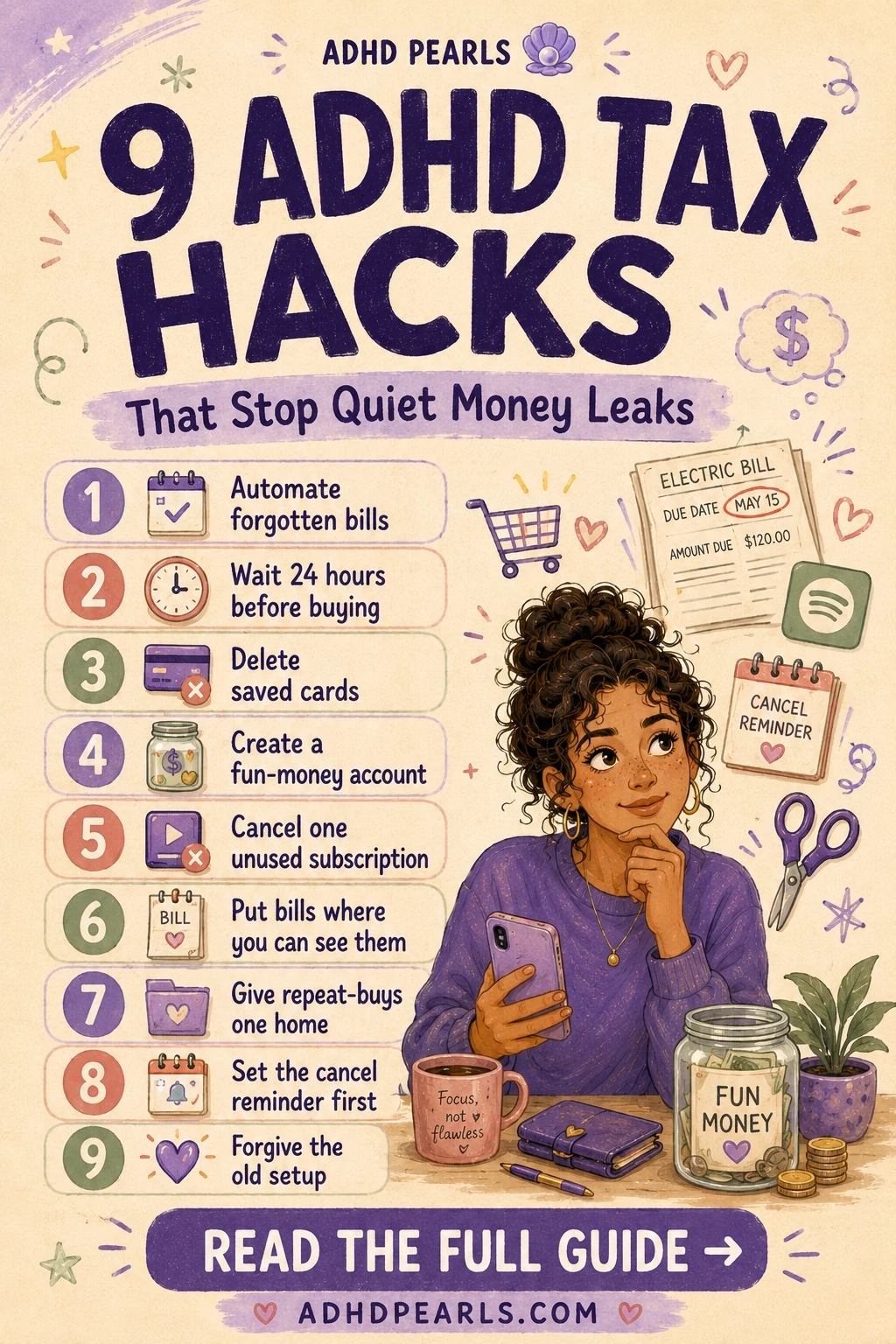

Here are the nine things that actually plugged the leaks for me — not by trying harder, but by changing the setup so my forgetful, dopamine-hungry brain had fewer ways to cost me money.

This article is personal and educational. It is not financial or medical advice. If debt or money stress is seriously affecting your life, please talk with a qualified financial professional and, about ADHD itself, a clinician.

Quick answer

What is the ADHD tax — and how do I stop paying it?

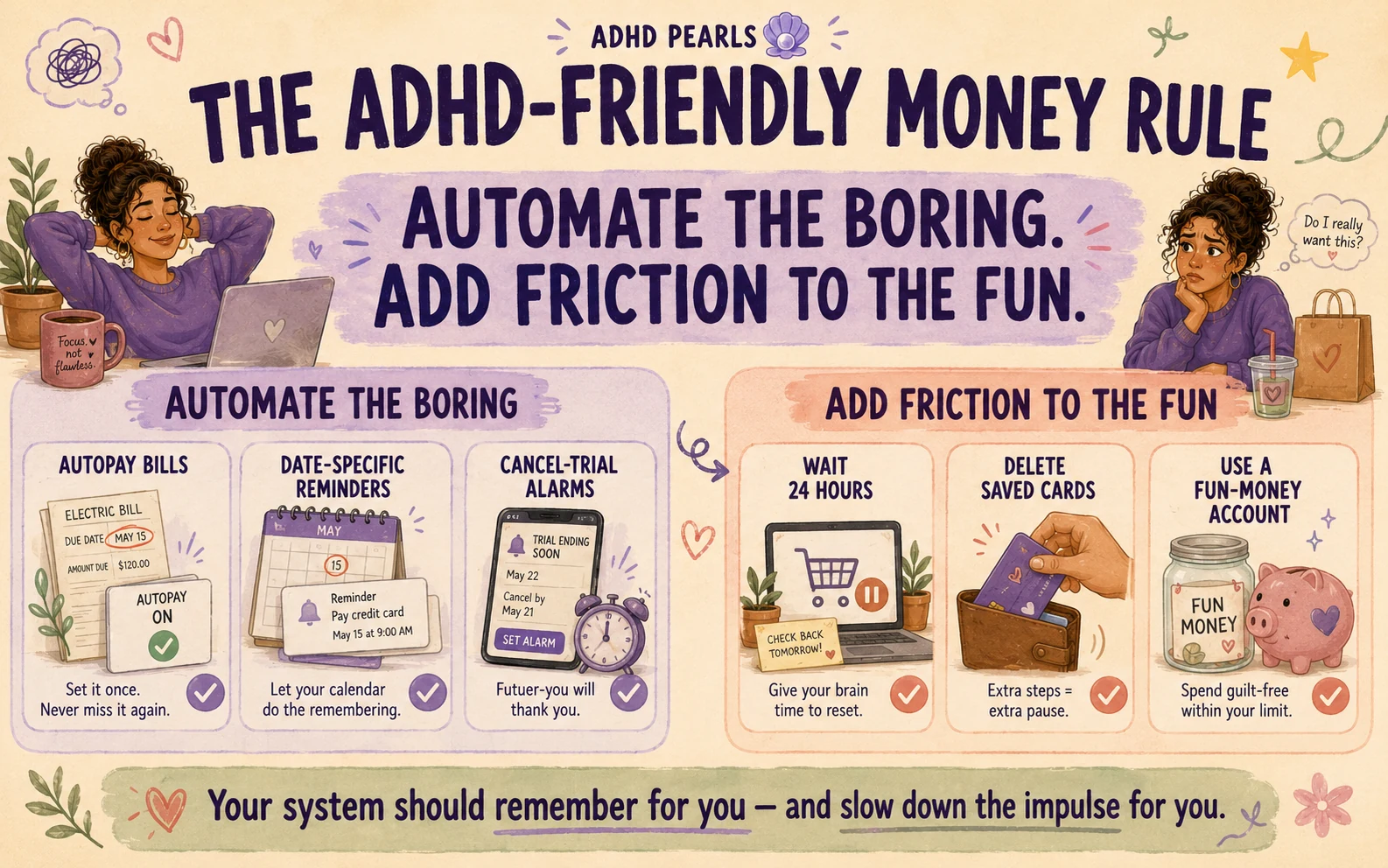

The ADHD tax is the recurring money you lose to late fees, impulse buys, forgotten subscriptions and re-buying things you already own — driven by impulsivity, time blindness and working-memory gaps, not carelessness. You stop paying it by changing the setup instead of your willpower: automate bills, add friction to spending (delete saved cards, wait 24 hours), corral impulse money in a separate account, and make bills impossible to miss.

One thing to be clear about: this isn't about becoming a frugal, spreadsheet-loving person who meal-preps their pennies. It's about stopping the quiet, automatic ways money slips out — so the same income goes further without you having to white-knuckle every purchase.

The ADHD tax often hides in late fees, impulse buys, forgotten subscriptions and duplicate purchases.

Key takeaways

📌The ADHD tax is the cost of executive-function differences, not a character flaw.

📌Research links ADHD to more impulse buying and missed payments — it's a real pattern.

📌Willpower fails at 11 p.m. Friction and automation don't.

📌Automate the boring stuff; add speed bumps to the fun stuff.

📌Shame keeps the cycle going. Forgiving the past tax helps you stop paying it.

Money asks your brain to do the exact things ADHD makes hardest: resist an impulse, remember a boring future task, and weigh a reward you can't feel yet against a cost that hasn't happened. Buying something delivers an instant hit of dopamine your brain is actively craving. Paying a bill on time delivers… nothing, until you forget and it delivers a fee.

This isn't just a vibe. Research has linked ADHD to higher rates of impulsive buying, breached credit limits, lower savings and missed payments — one analysis of UK bank data found adults with ADHD were roughly three times more likely to miss bill payments than people without it. So if money has always felt slipperier for you than it seems to be for everyone else, you weren't imagining it.

I wasn't bad with money. I was running a brain that finds "remember the invisible thing later" almost impossible, in a world that bills you for forgetting.

From ADHD Pearls

Free Stuck Reset

One tiny move for the moments you know what to do but still can't start.

My most expensive pattern was never not having the money. It was the bill being an invisible, boring, future task that my brain filed under "later" and then quietly deleted.

The fix is to take remembering off the table entirely. Put every fixed, non-negotiable bill — rent or mortgage, utilities, phone, insurance, minimum card payments — on autopay. Automation doesn't have an off day. It doesn't get distracted by a dog video. It just pays the thing.

One caution for low-balance weeks: only autopay what you can reliably cover, and keep a small buffer so autopay never causes an overdraft. The goal is fewer late fees, not a new way to get charged.

Tiny money move: Set up autopay on your single most-forgotten bill today.

2. Make “One Quick Thing” Wait 24 Hours

"I'll just quickly order this" is the money version of "I'll just quickly check my phone." At 11 p.m. it feels essential. By morning, I usually can't remember why a third water bottle was urgent.

So for anything non-essential, I make it wait 24 hours. Put it in the cart, then close the app. The wait isn't a punishment — it's a speed bump that lets the dopamine fade so you can decide with your actual brain. ADHD spending experts recommend exactly this, because the delay quietly dissolves a surprising number of "must-haves."

Tiny money move: Next time you're about to buy something you didn't plan, leave it in the cart for one sleep.

3. Delete Your Saved Cards

Confession: saved cards and one-tap pay turned "do I really want this?" into a thumbprint. The whole point of the technology is to remove the friction between wanting and buying — which is precisely the friction my brain needs.

So I deleted my card details from Amazon, the app stores and my browser. Now buying something means standing up, finding my wallet and typing sixteen digits — and somewhere in that small ordeal, the impulse often loses interest. Same logic for retail emails: unsubscribe, so the temptation stops arriving in the first place.

Tiny money move: Remove your saved card from the one shop you impulse-buy from most.

4. Give Impulse Spending Its Own Little Playpen

Trying to never impulse-spend again is a plan that lasts roughly until Tuesday. What works better is giving the impulse a boundary instead of banning it.

Open a small separate account — call it "fun money" or "me money" — and move a set amount into it each payday. That's the impulse budget. When it's gone, it's gone, but spending it never touches your rent. You get to be spontaneous inside a fence, which is far more doable for an ADHD brain than pure restraint.

And for the dopamine you're actually chasing, a free ADHD dopamine menu is a cheaper hit than checkout — a list of small, satisfying things that aren't your card.

Tiny money move: Decide one small weekly "fun money" number you could move into a separate account.

The ADHD-friendly money rule: automate the boring tasks and add friction to impulse spending.

5. Do the 10-Minute Subscription Autopsy

At one point I was paying for three streaming services I never opened, an app I used once, and a gym membership that functioned mainly as a monthly donation to my own optimism.

Subscriptions are the perfect ADHD-tax trap: invisible, automatic, and easy to forget because they never ask you to do anything. Once, go through your bank statement and your phone's subscription list and cancel everything you don't actively use. This is a hyperfocus-friendly task — set a 10-minute timer and make it a tiny treasure hunt for money you're already losing.

Tiny money move: Open your phone's subscriptions list right now and cancel one thing you forgot you had.

6. Put the Bills Where Your Eyes Already Go

For an ADHD brain, out of sight is genuinely out of mind. A bill in an email folder or a drawer doesn't exist. This is the same reason the "important paperwork" pile becomes archaeology.

So make the few things you can't automate impossible to miss. A visible note on the fridge, a recurring phone reminder for the exact due date (not "soon"), or a single sticky on your mirror. You're not relying on memory; you're putting the reminder physically in the path your eyes already travel.

Tiny money move: Set one dated phone reminder for your next non-automated bill.

7. Buy It Once, On Purpose

I own four pairs of scissors and can currently locate zero of them. The "I'll just buy another one" reflex is a real, recurring tax — you pay twice (or four times) for things you already own but can't find, plus all the little replacements for the charger, the umbrella, the specific pen.

Two fixes help. First, give the things you constantly re-buy one obvious home, so "I can't find it" stops triggering "I'll buy a new one." Second, when you do buy, buy the decent version once on purpose instead of the cheap version you'll replace three times. Paying for the same thing repeatedly is its own quiet tax.

Tiny money move: Pick one thing you keep re-buying and give it a single, visible home today.

8. Set the Cancel Reminder Before the Trial Starts

Free trials are designed around the assumption that you'll forget to cancel. For an ADHD brain, that's not an assumption — it's a near-certainty. "I'll remember in 30 days" is, historically, the funniest thing I tell myself.

So the moment you start a free trial, before you do anything else, set a reminder for two days before it ends — labelled "cancel [thing]." You're not trying to remember; you're handing the memory to a future alarm. If a trial needs a card up front, that reminder is the difference between free and an accidental annual subscription.

Tiny money move: On your next free trial, set the cancel reminder before you set up the account.

Free printable

Chasing a dopamine hit? Get a cheaper one than checkout.

The free ADHD Dopamine Menu is a list of small, satisfying things to reach for when your brain wants a hit — not a purchase.

Here's the quiet trap. Every time you notice money you lost — the fee, the duplicate, the year of an unused subscription — the shame spikes. And a brain flooded with shame does not make calm financial decisions. It avoids looking at the bank account at all, which is how the next late fee happens.

The version of me that started fixing this wasn't the one keeping score of past mistakes. It was the one who said: of course you forgot — your brain finds this genuinely hard, and now you're building systems that don't depend on remembering.

This isn't a soft add-on. Self-criticism tends to drive avoidance, and avoidance is where the ADHD tax thrives. If the money shame runs deep, the ADHD shame detox is a kinder place to start than another budget.

Tiny money move: Name one past ADHD-tax expense, then say out loud: that was the old setup, not a verdict on me.

At a glance

The 9 fixes

The fix

What it targets

Tiny money move

Automate bills

Forgotten payments

Autopay your most-forgotten bill

24-hour wait

Impulse buys

Leave it in the cart for one sleep

Delete saved cards

One-tap spending

Remove your card from one shop

Fun-money account

All-or-nothing restraint

Pick a weekly impulse number

Subscription autopsy

Invisible drains

Cancel one unused subscription

Visible bills

Out of sight, out of mind

Set one dated reminder

Buy once, on purpose

Re-buying & duplicates

Give one re-bought item a home

Cancel reminder first

Free-trial creep

Set it before you sign up

Forgive the past tax

Shame-driven avoidance

Reframe one past expense

If "just set up a system" is the part that never happens, you're not alone — that's the ADHD trap underneath the money one. The gentler entry points are the two-minute hacks for when you can't start and the phone hacks that cut the late-night scroll-to-checkout pipeline.

Save these ADHD money hacks for later

Save this ADHD tax guide to Pinterest so the nine money fixes are easy to find later.

FAQ: ADHD and Money

What is the ADHD tax?

The extra money you lose because of how ADHD symptoms play out — late fees on bills you could afford, impulse purchases, forgotten subscriptions and free trials, spoiled food, and re-buying things you own but can't find. It's not a real tax; it's the recurring cost of executive-function differences, and it can add up to a meaningful amount each year.

Why do ADHD brains struggle with money?

ADHD affects impulsivity, planning, working memory and the ability to weigh a future cost against a present reward — all of which money depends on. Buying gives a quick dopamine hit your brain craves; paying a bill on time is a boring future task that's easy to forget. The problem is rarely "not caring about money."

Is the ADHD tax real, or just an excuse?

It's real. Research links ADHD to higher rates of impulsive buying, missed payments and difficulty saving — one analysis found adults with ADHD were around three times more likely to miss bill payments. Naming it isn't an excuse; it's how you stop blaming your character and start changing the setup.

How do I stop impulse spending with ADHD?

Add friction and remove triggers instead of relying on willpower. Delete saved cards, unsubscribe from retail emails, wait 24 hours before non-essential buys, and keep a small separate "fun money" account so impulse spending has a boundary that never touches your bills.

Why do I forget to pay bills even when I have the money?

Because remembering the bill is the hard part, not affording it. A bill is an invisible, boring, future task with no urgency until it's a crisis — exactly what time blindness and working-memory gaps drop. Automating payments and making bills visually impossible to miss fixes the real problem.

When should I get help with ADHD and money?

If debt, overspending or financial stress is seriously affecting your daily life, sleep or relationships, talk with a qualified professional — a financial counsellor, and a clinician about the ADHD itself. These hacks reduce everyday leaks, but persistent money distress deserves real support.

You're not bad with money. You're running a brain that finds "remember the invisible thing later" genuinely hard — in a world that quietly charges you for forgetting. The fix was never a stricter budget. It was a setup that doesn't depend on a perfect memory or perfect restraint.

Pick one fix from this list and set it up today — autopay one bill, delete one saved card, cancel one subscription. That's the whole job. The money you stop losing adds up faster than you'd think.

For the woman who sets up the perfect system on Sunday and abandons it by Tuesday.

One short letter, every week. Real talk about ADHD, task paralysis, and the tiny wins that actually move the needle for a brain like yours. No shame. No hustle culture.